By Dr. Watson Scott Swail, President & Senior Research Scholar, Educational Policy Institute

I’m a broken record. I admit it. I’ve written about this issue several times recently. Some of our readers may suggest that one more time is far too many, but I simply cannot help myself because Bernie Sanders has struck again.

Yesterday, Senator Sanders, who is, for a second time, running for the Democratic leadership and Presidency, proposed a broad student debt forgiveness policy valued at $1.6 trillion. To put this number in perspective, the entire US federal budget is $4.1 trillion, which, by the way, outpaces federal revenues by almost a trillion dollars. But that is neither here nor there.

$1.6 trillion is a lot of money. And it truly hampers the lives of millions of Americans. As the Sanders camp estimates, 45 million Americans have some level of student debt, whether they graduated from college or not. Student debt is a serious problem, but the problem is not simply eliminated by withdrawing the debt of anyone who has a federal loan. For one, it assumes that people only have federally-funded debt. They do not. Millions of students have used credit cards and other means to help pay for college, so Sanders’ offer wouldn’t fully eliminate debt for students, although it would negate the largest piece of it. More importantly, the remission of debt would be a poor public policy that fails to solve much except to ease the financial pain for students and families. This is important, but not if it doesn’t get at the two central elements of the problem: college costs and state finances.

As stated, I’ve written about this issue as recently as May 21, 2019 in A Lot of Talk About a $40 Million Tuition Gift, in which I spoke about Robert Smith’s impassioned-but-perhaps-slightly-off-the-mark gift to 400 Morehouse graduates. I initially wrote about this four years ago when both Sanders and Hillary Clinton promoted the idea of free college. Please see An Open Letter to Senator Bernie Sanders: Your Free Tuition Policy is a Bad Idea. I wrote again on October 12, 2015 in The Broken Record of Student Debt, February 19, 2016 in A New Higher Education? Free Tuition? Again? Really?, and April 10, 2017 in New York Takes the First Dive into Free Tuition. I know, I know. I’ll try and stop.

Or, better yet, I’ll stop when they stop.

Without writing an overly long diatribe about this issue, I’ll shorten my thoughts and give you the basics on why this is a bad idea.

Some Basic Facts about Student Loan Debt

Here are some important statistics to consider for this discussion. These represent students attended a four-year public institution in 2015-16[1]:

- 47.4 percent took out a student loan; 64.8 percent received a grant; 6.5 percent of parents took out a PLUS Loan.

- The average loan was $7,500; the average grant was $7,400; the average PLUS loan was $12,800.

- The average cumulative loan amount for four-year public full-time students was $28,000, compared to $33,200 for those attending four-year private, non-profit institutions and $43,000 for those attending four-year private, for-profit institutions.[2]

- The average net price (not including loans) for four-year public students (doctorate-granting only) was $17,700.[3]

- There was little difference in the percentage of students who took out loans or the amount of loans by dependent/independent status and student/family income level.

- White students had higher net price than Black or Hispanic students, and dependent students had a higher net price than independent students.

- Dependent income had a high correlation with net price of institution. For example, a student with dependent income between $20k and $40k had an average net price of $16,200 compared to $22,900 for those with incomes above $100,000.

In addition:

- The average undergraduate tuition and fee charges for full-time students at a four-year public institution increased 13 percent between 2010-11 and 2017-18 (after adjusting for inflation)[4] from $8,000 to $9,000.

- The percent of four-year public full-time students taking on debt declined between 2010-11 and 2016-17 by 4 percent (from 50 to 46 percent).

- The average annual loan amount for full-time students at four-year public institutions remained constant between 2010-11 and 2016-17 at about $7,000.

- Low-income students (lowest quartile) had an average net price of $14,800 compared to $21,300 for affluent students (highest quartile) in 2015-16.[5]

Commentary

First, let us understand that student loans—in isolation—are not a bad thing. They may be a necessary evil, but evil, in this case, is not always bad. As the data above illustrate, there are extremes, but, on average, student debt isn’t the avalanche that many make it out to be. It is a serious issue and, for some, is crushing. We always remind readers that averages cloak the extremes, while the extremes are used anecdotally to diminish or promote an issue. Be mindful of data.

It is helpful to understand and remember that federal student loans, such as the Stafford subsidized and unsubsidized loans, were created and designed to help students who could not have gone to college earn a postsecondary credential without such support. Most students, up until recently, have been able to do so with a modest level of student debt. The highest debt loads have traditionally been held by people in medicine and other long-term, very expensive education programs. But even though those individuals had high student debt, the overarching sense was that they would enjoy the income to repay their debt.

So, let’s be clear: student loans serve an important service to equity and opportunity.

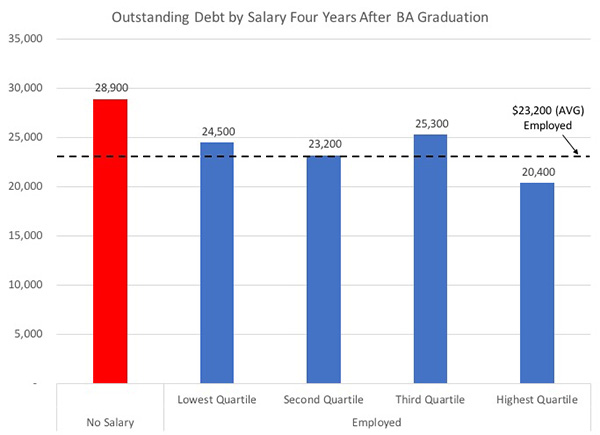

Still, people stressed with large debt burdens have a difficult road, and we should be mindful of this issue. The illustration below reminds us that, even four years after graduation, graduates owe a fair bit of loan debt, and those that are unemployed have an even higher debt burden due, in large part, to compounding interest.

SOURCE: Cataldi, E.F., Staklis, S., and Woo, J. (2018). Four Years Later: 2007-08 College Graduates’ Employment, Debt, and Enrollment in 2012. Stats in Brief. U.S. Department of Education, National Center for Education Statistics (NCES 2018-435). Data from Baccalaureate and Beyond Longitudinal Study (B&B:08/12).

NOTE: Those who earned $1–$31,199 were the 25 percent of bachelor’s degree recipients with the lowest annualized salary; those who earned $31,200–$42,999 were the 25 percent of bachelor’s degree recipients with lower middle annualized salary; those who earned $43,000–$59,999 were the 25 percent of bachelor’s degree recipients with higher middle annualized salary; and those who earned $60,000 or more were the 25 percent of bachelor’s degree recipients with the highest annualized salary.

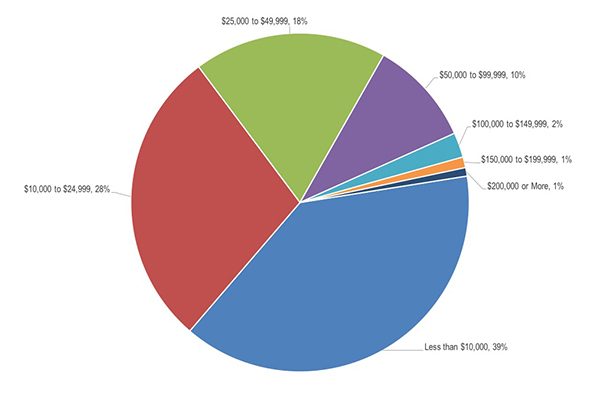

Also important to know is not all student loan debtors have large debts. The graphic below from The College Board in 2014 shows us that 39 percent of students who have student loan debt owed less than $10,000. Two thirds of all borrowers had loan debt under $25,000. And only 15 percent of students had loan debt above $50,000. This is important to remember in this conversation. Only a small portion of students were deeply saddled with debt, although we must remain mindful that debt is relative to income.

SOURCE: The College Board Trends in Higher Education; Federal Reserve Bank of New York Consumer Credit Panel/Equifax.

With these data in hand, here are a few points:

One. Eliminating the debt of 45 million people would send an imprudent message to students that financial decisions do not matter. If one chooses to attend an overly expensive school, the taxpayers, via the federal government, will cover your losses. There will be no penalty for decisionmaking. As in life, we make certain decisions based on our ability to pay and take on debt that we agree to repay based off our future increased earnings. Although the free college idea being floated around is laudable on one level, it is both too costly and fails to have a buy-in for students for the cost and price of college. Our system is based on shared responsibility. We can question whether the share is unfairly distributed between those who can pay and those who cannot, but there always exist a shared relationship involved in postsecondary education funding. And while we are at it, ask the Irish how their free tuition program went (spoiler: not so well).

Two. As with Bernie Sanders proposal, there are no income limits on who would receive this benefit, although Senator Warren’s proposal does appropriately impose an income limit. Thus, Sanders’ policy greatly benefits those who have the financial means to pay their debt. We call these policies “regressive,” as they tend to benefit those at the upper limits of the income distribution. In other words, it rewards affluent students and families at great cost to taxpayers.

Three. Sanders’ policy lets postsecondary institutions and state legislatures off the hook. Public college pricing is primarily a state-controlled issue. The state has the mandate for providing a public postsecondary system and provides the necessary subsidies to colleges and universities through state budgets. In addition, they have either total or partial control (varies greatly by state) of the tuition and fee levels set at public institutions. According to Illinois State University, an estimated $92.6 billion was appropriated by states in 2018-19 for higher education.[6] Compared to the $78.6 billion provided in 2009-10 and adjusted for inflation, states have been able to keep pace in recent years. However, during that time, the “cost” of providing a higher education has also risen, and institutions have increased tuition and fees disproportionally to make up the gap between funding and cost. Between 2000-01 and 2017-18, tuition and fee charges at public four-year institutions doubled from $5,031 to $9,970 (adjusted for inflation using 2017 dollars). If debt is simply wiped away, the colleges, universities, and legislatures are scot-free on curtailing college costs and providing the necessary resources for a higher education. The message is clear: costs do not matter because taxpayers will absorb the increases.

Four. It would bankrupt the country. Senator Sanders has listed how he would raise $2 trillion over 10 years to pay for the program through new taxes aimed at Wall Street largesse. The problem is that the debt issue will continue to get bigger as college becomes more expensive, which is surely will since there is little motivation to curtail cost increases (see prior point). At a time when the country is hemorrhaging money, has a $21 trillion debt itself, and is entertaining universal health care, something that would benefit all citizens, the cost of either/both free college and debt forgiveness is untenable.

To provide some context for the above, let me state my own history as anecdote. Most people do not know that I am a first-generation college student. My parents did not go to college, with the exception of my dad for one year. We grew up knowing we were “expected” to go to college, though, which is critically important to eventual matriculation. My postsecondary route included two years at a community college, two years at university, and living at home throughout my undergraduate experience, which did take five years due to a change in major. My parents covered room and board; I covered everything else and worked 2-3 jobs during school and summer to support myself. Upon graduation, I worked as a teacher for five years, then completed my masters abroad (in the US) on my own dime with pocket money from my brothers and parents (meaning, I still paid for tuition, fees, and room and board). I worked again as a teacher, then moved to DC where I completed my doctorate in 2.5 years at a very expensive private school by way of a 20-hour/week work study. I worked the other 20 hours as well, so basically worked full time and studied full time. My days started at 5:30am and ended at about 10pm during the week. This I did with a small, young family.

My point is simple: I made choices and things worked out fabulously for me. I was fortunate, but I was also dedicated and focused. For playback purposes, I went public, public, public, private. Or… low cost, low cost, low cost, high cost. I worked my way up, stopped to earn money in between degree programs, and made it work and ended up with a terminal degree and modest debt that I paid back in literally two years. That was two decades ago. College is more expensive now. The situation is tougher for students. But if college was free or cheaper, I would have made different decisions. Better? Not so sure.

To be clear, we need to have universal policies that reduce the burdens put on students, especially those from low- and middle-income families. There is no argument here. But prudent public policy to do so will need to incentivizes institutions to hold down the cost of a higher education, encourage state legislators to provide necessary funds for postsecondary systems, and continue to require students to bear part of the responsibility for their higher learning.

[1] https://nces.ed.gov/pubs2018/2018466.pdf.

[2] https://nces.ed.gov/programs/coe/indicator_cub.asp.

[3] https://nces.ed.gov/pubs2019/2019475.pdf.

[4] https://nces.ed.gov/programs/coe/indicator_cub.asp.