By Watson Scott Swail, President & Senior Research Scholar, Educational Policy Institute

Back in 1971, the FRAM oil filter company introduced what would become a very popular commercial on TV that ended with this tag line: “You can pay me now, or pay me later.” The meaning being that the cost of a $10 oil filter could save you hundreds or thousands of dollars down the road.

Today, due primarily to the high cost of college, but also in the reduced amount in family savings, more students than ever are choosing to pay for their college later than now. For most students, this is not a choice. Student loans are a necessary evil for over two thirds of the college-going population. And while access to loans is a good thing, too much loan debt can be detrimental, especially for people who fail to complete their studies. Today’s Swail Letter looks at the issue of student debt and the retirement population.

In 2016, over 3 million youth graduated from high school in the United States. Of those, 70 percent, or 2.2 million, matriculated directly to college.[1] More women than men; more Whites than Blacks and Hispanics. Still, over two-thirds of our high school graduates matriculated directly to college: the highest percentage in the history of our nation.

The evidence of return to a college education is pervasive and well known, however overemphasized the adage often is. People who go to college earn more than people who do not. And people who earn professional and graduate degrees earn even more. These facts are indisputable and people like me have been extolling these virtues for years. College graduates live longer, live better; go on more vacations and have more time off; and have better health care, more investments, and increased retirement savings.

All of this discussion, however, depends largely on definition. The highest returns to a college education go to the highest educated as well as those who go to the “best” schools. Conversely, the lowest returns go to those with the lowest levels of college education. Not all is equal, and not all is average. Some do better; some lesser. This is the American Way.

Of great concern to me, with regard to public policy, is the debt burdens of graduate and non-graduate students. We often think of debt with college graduates, but non-graduates have large debts, too. As I often say to colleagues at our workshops, the challenge that dropouts have is that they have significant debt to repay but lack the parchment — the college degree — to help pay for it. Their earning potential is only slightly—if at all—better than when they started school, but they lack the credential to increase their material wellbeing.

According to a recent piece in Time, the number of students securing student loans has tripled in the last decade. Over 70 percent of graduates have significant loan debt totaling nearly $1.5 trillion. One in four adults in the US are paying off a student loan for themselves, their children, or their grandchildren, averaging $37,000.[2]

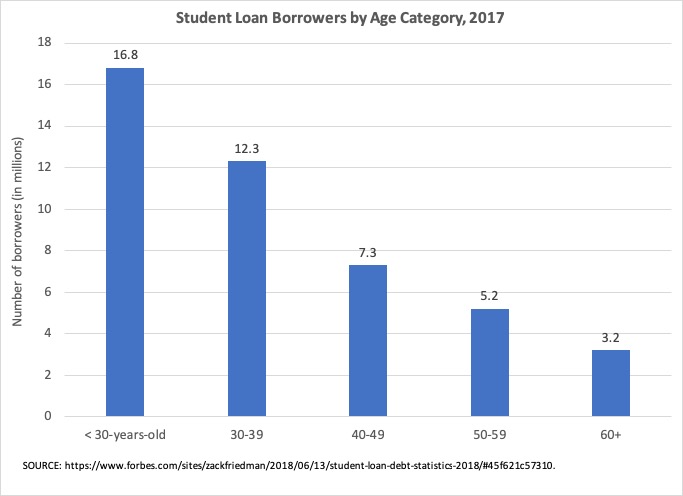

Most student borrowers are younger. According to the Federal Reserve Bank of New York, 38 percent of borrowers are under 30 years of age, and 65 percent are under the age of 40. While the percentage of borrowers who are above 50 and even above 60 seems small, it is certainly not negligible. Seven percent of all borrowers, representing 3.2 million people, are over the age of 60. One fact is tremendously important: one quarter of retirees aged 65 to 74 and over half of those over the age of 75 have a defaulted student loan. This compares to only 12 percent of those under age 50.[3]

The AARP is worried about the potential ramifications of student debt. “We consider it a looming threat,” is what Lori Trawinski of the AARP Public Policy Institute said about the issue.[4] Looming debt impacts how people save and prepare for retirement.

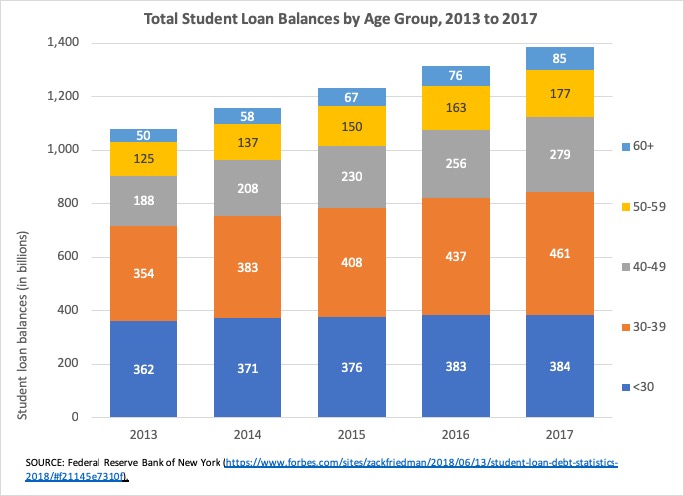

The average student debt of older borrowers is over $23,000 and over 100,000 of these borrowers had wage garnishments to collect debt funds.[5] The graphic below illustrates the total loan balance by age group from 2013 to 2017. Although the 60+ group is the smallest, the level of debt has risen 71 percent during this four-year period from 50 to 85 billion. These levels and rates will continue to escalate as the baby boomers get increasingly older.

Student debt impacts how people save and invest. The Center for Retirement Research at Boston College found that millennials with student loans save half as much for retirement by age 30 as those without.[6] And the LIMRA Secure Retirement Institute found that an outstanding student loan debt of $30,000 reduced retirement savings by $325,000; $50,000 of debt reduced savings by over half a million dollars.[7]

While we cannot say how this will all play out in future years, the trends are dire for aging Americans. The problems and solutions are equally complex. Over the past several decades, earnings have stagnated while living costs have increased. Individuals are paying more in either taxes or faux taxes in the form of “fees” (e.g., car tag fees; building permits; fines and penalties). Even health care premiums have had a dramatic impact on savings potential. The average US family pays over $13,000/year in premiums with an added annual deductible of $8,803.[8] Thus, many families pay an additional $20,000 in health care costs that would effectively be considered a tax in other western, industrialized nations.

Free tuition proposals could help, but tuition rarely amounts to over half the cost of an education. As more people go to college, the impact of free tuition on the government budget would be potentially devastating. Improved use of Income Contingent Loans could help mitigate the long-term penalty afforded by large loan debt, but that has a high cost as well. Realistically, there are no solutions for current loan borrowers with significant debt, and the future will bring more retirees working late into their 70s or going on to government assistance than ever before.

We have to figure if we want to pay the bill now or pay it later. For some people, there exists a limited set of choices. Go to college or not go. Go to a costlier college or a less-costly college. Go part-time or full-time. For others, there are standard-of-life issues that can be limited to decrease debt. In the end, we cannot achieve equity in college going and college costs. It may be desired, but it is an impossible goal to attain. Thus, our real goal is to reduce the gaps in access and cost as much as possible between not just the poor and the affluent, but the middle class that takes a major financial blow.

[1] https://www.bls.gov/opub/ted/2017/69-point-7-percent-of-2016-high-school-graduates-enrolled-in-college-in-october-2016.htm

[2] https://www.cnbc.com/2018/02/15/heres-how-much-the-average-student-loan-borrower-owes-when-they-graduate.html.

[3] https://loans.usnews.com/more-seniors-carry-student-loan-debt-into-retirement

[4] https://www.politico.com/agenda/story/2018/06/07/student-loans-debt-aarp-000666

[5] https://www.aarp.org/money/credit-loans-debt/info-2017/student-loans-debt-repayment-retirement.html

[6] http://time.com/money/5419581/a-simple-trick-to-pay-down-student-debt-and-save-for-retirement-at-the-same-time/

[7] https://www.moneytips.com/student-debt-results-in-loss-of-retirement-savings/542

[8] https://www.ehealthinsurance.com/resources/affordable-care-act/much-health-insurance-cost-without-subsidy

Great post thhank you